Yes. This post really is about how to handle the tax obligations that arise from having a household employee, such as a housekeeper or nanny.

It will not be interesting.

It will not be funny.

But, if you are fortunate enough to have paid help at home, it may contain some information you can use. This is the time of year you need to be preparing, filing, and paying things that relate to any household employees you had in 2013. And, if you’ve been lax about these issues in the past, the new year is the perfect time to turn over a new leaf. [hr]

Do I Really Have an Employee?

That is the threshold question, and the answer is: you might. The Internal Revenue Service uses a number of factors to determine whether a person who works in your home is an employee (for whom you have tax withholding and reporting obligations) or an independent contractor (for whom you are off the hook). In general, a worker is your employee if you control what work is done and how it is done.

For purposes of determining whether a person is an employee, it does not matter whether the work is full time or part time, or that you hired the worker through an agency. It also does not matter whether you pay the worker on an hourly, daily, or weekly basis, or by the job. More importantly, it doesn’t matter whether you and the worker “just agree” that the worker is an independent contractor. The legal test controls, regardless of how you and the worker prefer to define your arrangement.

Every situation is different, but an example illustrates the difference between an employee and an independent contractor.

A family hires a worker to clean their house once a week. The worker is scheduled to work on Wednesdays, but from time to time she reschedules to a different day. Sometimes, rather than cleaning the house herself, she unilaterally sends her sister or niece to do the work. She makes her own schedule, with the understanding that she will perform her work during the normal work day. She holds herself out as available for other work, and there is no expectation that she is available exclusively to the family. That is to say, when she is not working for the family, she’s cleaning other people’s houses. In this situation, I am pretty comfortable that the worker is an independent contractor.

The same family also has a nanny. The nanny is required to arrive each morning by 8 a.m., and she stays with the children until the first parent arrives home around 6 p.m. She follows specific guidelines about the children’s care. She cannot reschedule, and she cannot send another person in her stead. While she might pick up the occasional babysitting gig on the side, she does not (and cannot) do other work that conflicts with her taking care of the family’s children. On these facts, I’d have a hard time arguing that the nanny was not an employee.

Don’t freak out yet. There is a de minimis rule that prevents people who just have the occasional Saturday-night babysitter from having to deal with taxes and reporting. You have to pay federal unemployment tax (discussed below) only if you pay $1,000 or more in any calendar quarter to household employees. You have to withhold and pay social security and Medicare taxes (discussed below) only if you pay $1,900 or more in 2014 ($1,800 or more for 2013) to any one household employee. If you only shell out $60 a month for child care during your monthly date nights ($180 per quarter and $720 per year), you’ll never trip over these lines.

However, if the person who works in your home is an employee and your payments are over the thresholds, you must report certain information to the Internal Revenue Service and Social Security Administration, and must withhold and pay certain taxes to the government. [hr]

Taxes? What Taxes?

In Texas, when dealing with household employees, three types of taxes are in play: federal income tax, federal employment taxes, and unemployment taxes. Let’s take them in order.

Federal income tax is probably what comes to mind when you think about taxes. In general, income taxes are withheld from the pay a worker otherwise earned. The employer remits the withheld money to the government, to go towards the worker’s current-year income tax liability. Unlike most other employers, as a household employer, you are NOT required to withhold federal income tax. You are allowed to withhold it if your employee asks you to. If you withhold, the employee’s federal income taxes require some bookkeeping on your part, but because they come out of money you already owe your employee, they don’t take any additional jingle out of your pocket.

The term “employment taxes” is a catch-all term that applies to three types of tax: social security, Medicare, and unemployment. Social security tax pays for old-age, survivors, and disability benefits for workers and their families (hence the name, “Social security tax”). Medicare tax pays for hospital insurance (Get it? “Medicare.”). Together, these taxes are referred to as Federal Insurance Contributions Act (“FICA”) taxes. Both you and your employee may owe FICA taxes. Each person’s share is 7.65% (6.2% for social security tax and 1.45% for Medicare tax) of the employee’s wages. It’s important to understand that your share does NOT come out of your employee’s paycheck. It comes out of your pocket. You can withhold your employee’s share from her wages or opt to pay it yourself (in which case, it’s additional money out of your pocket).

The term “employment taxes” is a catch-all term that applies to three types of tax: social security, Medicare, and unemployment. Social security tax pays for old-age, survivors, and disability benefits for workers and their families (hence the name, “Social security tax”). Medicare tax pays for hospital insurance (Get it? “Medicare.”). Together, these taxes are referred to as Federal Insurance Contributions Act (“FICA”) taxes. Both you and your employee may owe FICA taxes. Each person’s share is 7.65% (6.2% for social security tax and 1.45% for Medicare tax) of the employee’s wages. It’s important to understand that your share does NOT come out of your employee’s paycheck. It comes out of your pocket. You can withhold your employee’s share from her wages or opt to pay it yourself (in which case, it’s additional money out of your pocket).

Unemployment taxes are paid at both the federal and state level. They are used to pay unemployment compensation to workers who lose their jobs. Federal unemployment taxes are referred to as Federal Unemployment Tax Act (“FUTA”) taxes. The FUTA tax is 6% of your employee’s FUTA wages, up to $7,000. It’s not withheld from your employee’s wages, so it’s on you–the employer–not the employee. All or a portion of the amounts you pay to the state unemployment fund by April 15 of the following year are credited against your federal liability, resulting in a net federal rate of only 0.6 percent. Don’t get dizzy on the fractions. Just understand that you need to pay money to the Texas Workforce Commission by April 15 of the following year, and the money you pay will show up as a credit against FUTA liability on your personal federal return. [hr]

Decisions, Decisions.

This is the single trickiest part of the entire process: both personally and arithmetically. As a household employer, you can decide to pay your employee’s FICA taxes on her behalf rather than withhold it from her pay. That is to say, in addition to paying your 7.65% employer-share of FICA taxes, you can pay your employee’s 7.65% employee-share of FICA taxes, causing yourself–rather than your employee–to be out of pocket for this amount.

Why would you do this? Eh, if you’re like me, you didn’t clue into all of this until after you’d agreed to pay your child’s caretaker a particular rate, and you felt bad giving her a haircut you knew she didn’t expect. If you’re a Good Person, you might do it because you believe your employee needs the money more than you do.

If you decide to pay your household employee’s FICA taxes on her behalf, the amount you pay on her behalf IS included in her wages on the Form W-2 you prepare (and for purposes of any income tax you withhold), but it is NOT itself subject to FICA or FUTA taxes. As a result, your employee’s Form W-2 will show her actual wages as the social security and Medicare wages (used as the base for calculating FICA taxes) but will show her actual wages plus the FICA tax you paid on her behalf as her total wages (used to calculate her income tax liability).[hr]

How Do I Report All of This and Pay all the Taxes?

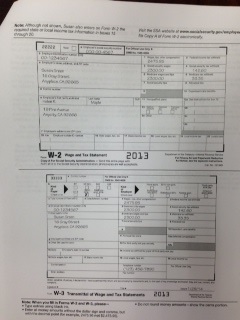

You must file a Form W-2 for each employee. You must give each employee her copy of the Form W-2 by January 31 of the following year. You must send a copy of each Form W-2, together with a Form W-3 to the Social Security Administration by February 28 of the following year. Note: you do not use your Social Security Number on these forms. You need to obtain an Employer Identification Number from the Internal Revenue Service, which you can do on-line. Bottom line: computer systems are unpredictable; don’t wait until the last minute.

You must file a Form W-2 for each employee. You must give each employee her copy of the Form W-2 by January 31 of the following year. You must send a copy of each Form W-2, together with a Form W-3 to the Social Security Administration by February 28 of the following year. Note: you do not use your Social Security Number on these forms. You need to obtain an Employer Identification Number from the Internal Revenue Service, which you can do on-line. Bottom line: computer systems are unpredictable; don’t wait until the last minute.

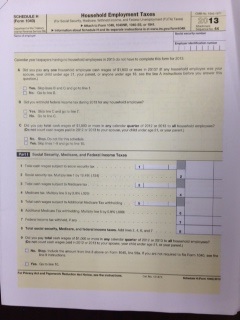

The Forms W-2 and W-3 are information returns. They tell the Internal Revenue Service about the employee’s income (so that it can be checked against what the employee reports on her personal income tax return) and tell the Social Security Administration about the employee’s Social Security payments (so that those amounts are credited to the employee’s eventual Social Security benefits). The taxes (and any of your employee’s income tax that you withheld) are reported using Schedule H, Household Employment Taxes, which is attached to your personal income tax return (Form 1040). The total amount on Schedule H flows through to your return and is added to your other income tax liability. If you roll like I do, know that Schedule H preparation is included in the Deluxe version of Turbo Tax.

The Forms W-2 and W-3 are information returns. They tell the Internal Revenue Service about the employee’s income (so that it can be checked against what the employee reports on her personal income tax return) and tell the Social Security Administration about the employee’s Social Security payments (so that those amounts are credited to the employee’s eventual Social Security benefits). The taxes (and any of your employee’s income tax that you withheld) are reported using Schedule H, Household Employment Taxes, which is attached to your personal income tax return (Form 1040). The total amount on Schedule H flows through to your return and is added to your other income tax liability. If you roll like I do, know that Schedule H preparation is included in the Deluxe version of Turbo Tax.

State unemployment taxes are reported and paid through the Texas Workforce Commission website. You’ll need to set up an account.[hr]

A Few Tips.

I work with the Internal Revenue Service every day and have tremendous respect for the work they do to administer our country’s tax laws. Still, the first time I went through this process, I found it very challenging–enough to make even the most diligent taxpayer want to throw up her hands. I have a few practical tips that might help you.

First, understand that this post is for informational purposes only, to help you understand where the ditches are. At the very least, read the Internal Revenue Service Publication 926, Household Employer’s Tax Guide. If your situation is complicated or you have questions, consult your tax advisor.

First, understand that this post is for informational purposes only, to help you understand where the ditches are. At the very least, read the Internal Revenue Service Publication 926, Household Employer’s Tax Guide. If your situation is complicated or you have questions, consult your tax advisor.

Second, be aware that you must file Forms W-2 and W-3 by paper, and that the forms cannot be printed off the internet. You can contact the Internal Revenue Service to have forms mailed to you or–if it’s getting down to the wire–pick up blank forms at the Internal Revenue Service Taxpayer Assistance Center located near the airport. You will make mistakes. Grab multiple copies of the forms.

If you use a professional return preparer and choose to pay FICA taxes on your employee’s behalf, check the preparer’s work. I’ve seen multiple instances of a return preparer bungling the math in this situation.

Understand that the various taxes accrue during the year but are payable in the next year, together with your own income tax liability. To avoid coming up short, have a plan for where that cash is going to come from. One option is to estimate the liability as it accrues and tuck that amount of money away in a savings account or other place you won’t touch it, so that it’s there when you need it. Another (more foolproof?) option is to provide your employer with a new Form W-4 to increase the amount withheld from your own paycheck. (Form W-4 was in that huge stack of paperwork you filled out when you started your job. It’s the form that tells your employer how much income tax to withhold from each of your paychecks. You can adjust your withholdings by giving your employer a new one at any time.) The money will be sent to the Internal Revenue Service as it is withheld during the year. It will be reflected on your own Form W-2 and become like a credit on your personal income tax return.[hr]

Can’t I Just…You Know…Not Worry About This?

There is nothing easy or fun about household employee taxes. It’s a lot of paperwork and money out of your pocket. It’s very tempting to…focus on other things.

Our tax system depends on individual compliance. It’s incumbent upon all of us to correctly report and pay our tax liabilities. More importantly, the social security taxes you and your employee pay are used to calculate your employee’s or her family’s eventual social security benefits. Our household employees take care of our children, clean our homes, and–in many cases–depend on us for their livelihoods. To me, that relationship creates a moral obligation to ensure we do our part to protect them in their later years.

Don’t be Zoe Baird. Life is long, and you never know when your personal taxes might become a matter of national importance. The costs of compliance really aren’t that high, and it’s just not worth cutting corners.

[hr]

Can We Stop Talking About This Now?

Yes. [hr]

The information in this post is current as of January 20, 2014. It is for general information purposes and should not be construed as legal, accounting, or other advice.

")

{kind=link}